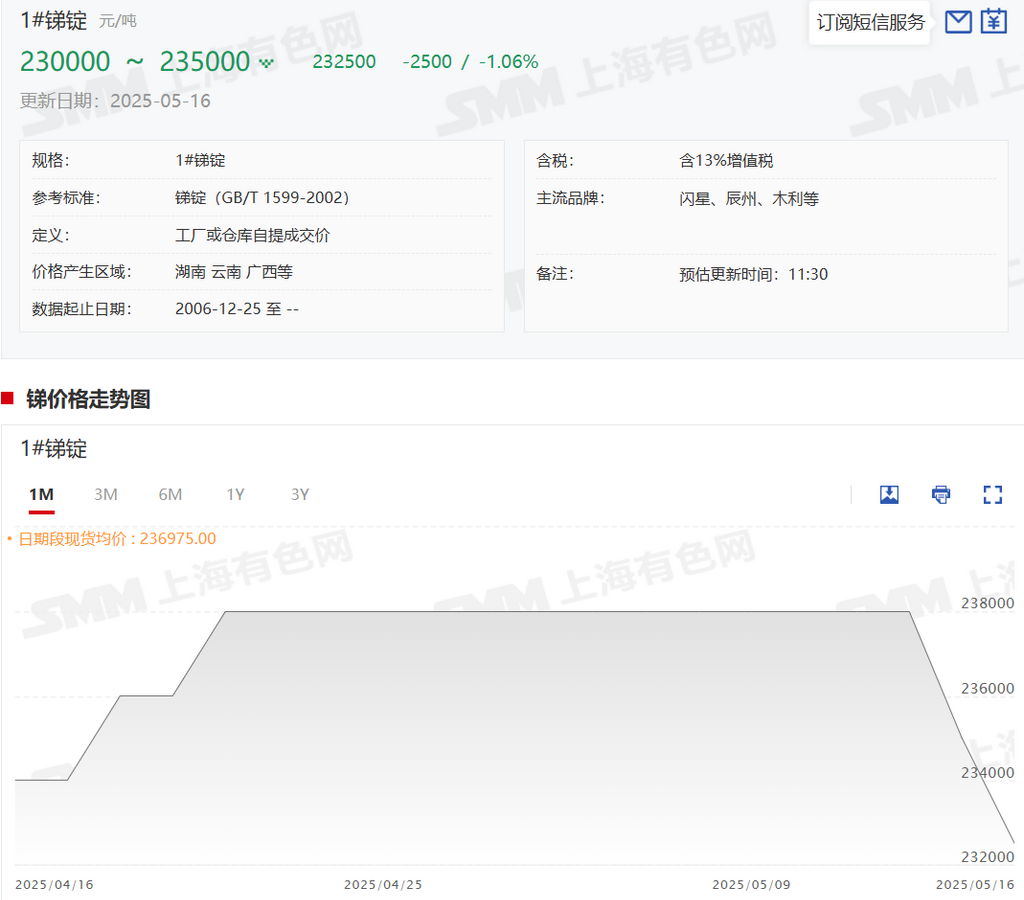

SMM News on May 16: After a prolonged period of stability and firmness, antimony prices experienced a certain decline this week. Although the fundamental supply and demand dynamics in the antimony market have remained relatively unchanged, the significant suspension of imported ore entering the domestic market has led to a severe shortage of domestic antimony raw materials. Additionally, the overall inventory of antimony products among domestic manufacturers is at historically low levels, prompting manufacturers to continue stabilizing their quotes. In the domestic end-use market for antimony products, whether for flame retardants or PV applications, orders have remained basically stable. Although there has been no recent improvement in orders from the end-user side, they have also not deteriorated, with an overall good pace of just-in-time procurement. However, due to the recent intermingling of bullish and bearish market news, the sentiment in the hot money market has become chaotic, leading to the entry of some low-priced supplies into the market. As of now, the SMM average prices for antimony are as follows: 2# low-bismuth antimony ingot at 228,500 yuan/mt, 1# antimony ingot at 232,500 yuan/mt, 0# antimony ingot at 236,500 yuan/mt, and the average price for 2# high-bismuth antimony ingot at 225,500 yuan/mt. As for the market prices of antimony trioxide this week, as of now, the SMM average prices for antimony trioxide are: 99.5% purity at 198,500 yuan/mt and 99.8% purity at 210,000 yuan/mt.

Additionally, according to SMM's assessment, the overall production of antimony ingots (including antimony ingots, crude antimony conversion, antimony cathode, etc.) in China in April 2025 is expected to decline significantly by around 10% MoM compared to the previous month. Specifically, among the 33 surveyed entities currently assessed by SMM, 8 manufacturers have halted production, a decrease of 4 from the previous month; 21 manufacturers have experienced a reduction in production, an increase of 4 from the previous month; and 4 manufacturers have maintained basically normal production levels, unchanged from the previous month. From the perspective of antimony ingot production, antimony production in April declined again after rebounding in March, a phenomenon considered normal by many market participants. This is attributed to the ongoing inability of many overseas ore sources to enter the domestic market, coupled with the poor progress of mining operations at northern ore sources, with many mines still in the process of gradual recovery or remaining suspended. Currently, many market participants indicate that the overall supply of domestic raw materials remains tight, and the reluctance of antimony ore suppliers to sell is still evident. Many manufacturers state that their current inventory levels are still in a phase of reduction. If the future increase in domestic mine raw material supply can alleviate the raw material shortage, production in May may show signs of recovery; otherwise, the reduction in market inventory will continue. Market participants anticipate that the national antimony ingot production in May 2025 is likely to decline compared to April, although a stable production level is also a possibility. However, based on the current situation, the likelihood of an increase appears relatively small. Furthermore, according to SMM's assessment, the production of first-grade sodium pyroantimonate in China in April 2025 is expected to decline by around 1.8% MoM compared to the previous month, remaining basically stable after a significant rebound in the previous month. Many market participants consider this a normal phenomenon. Since antimony prices began to rise continuously from the end of February, orders for glass factories have also started to increase. The production increase of many manufacturers in March was also related to receiving more orders, and it is reasonable for this situation to continue into April. Looking at other detailed data, among the 11 survey respondents from SMM, in April, 2 manufacturers were in a state of shutdown or commissioning, 4 sodium pyroantimonate manufacturers experienced an increase in production, and 2 manufacturers saw a significant decline in production. As a result, the overall production remained basically stable, with a slight decline. Market participants expect that the national production of sodium pyroantimonate in May is unlikely to continue to decline compared to April, and it is more likely to remain flat or increase slightly.